The UK Life Sciences Ecosystem

In 2020 JPG assessed the strengths and weaknesses of the UK R&D ecosystem, as seen through the lens of colleagues working on R&D programmes in the UK. This included consideration of improvements that would be valued and key competitor countries in different parts of what we consider to be the UK Value Chain.

In the course this exercise we found there was low awareness of UK Life Sciences policy in the Japanese R&D community. To address this, we have collaborated with Government on a number of roundtable events attended by global heads of research and development. More information is on the Innovation and Investment page.

An update to the original 2020 report was conducted in 2023. Both 2020 and 2023 reports are summarised below. Full reports can be downloaded as indicated.

Overview – about this project

In 2020 the JPG conducted a comprehensive review of the UK Life Sciences ecosystem from the perspective of the Japanese industry.

In 2023 we have undertaken an exercise to explore any changes in perception over the last three years

We are keen to explore ways in which we can work with other system players to leverage UK strengths to attract inward investment and increase awareness of the UK offer in Japan.

Key findings since 2020

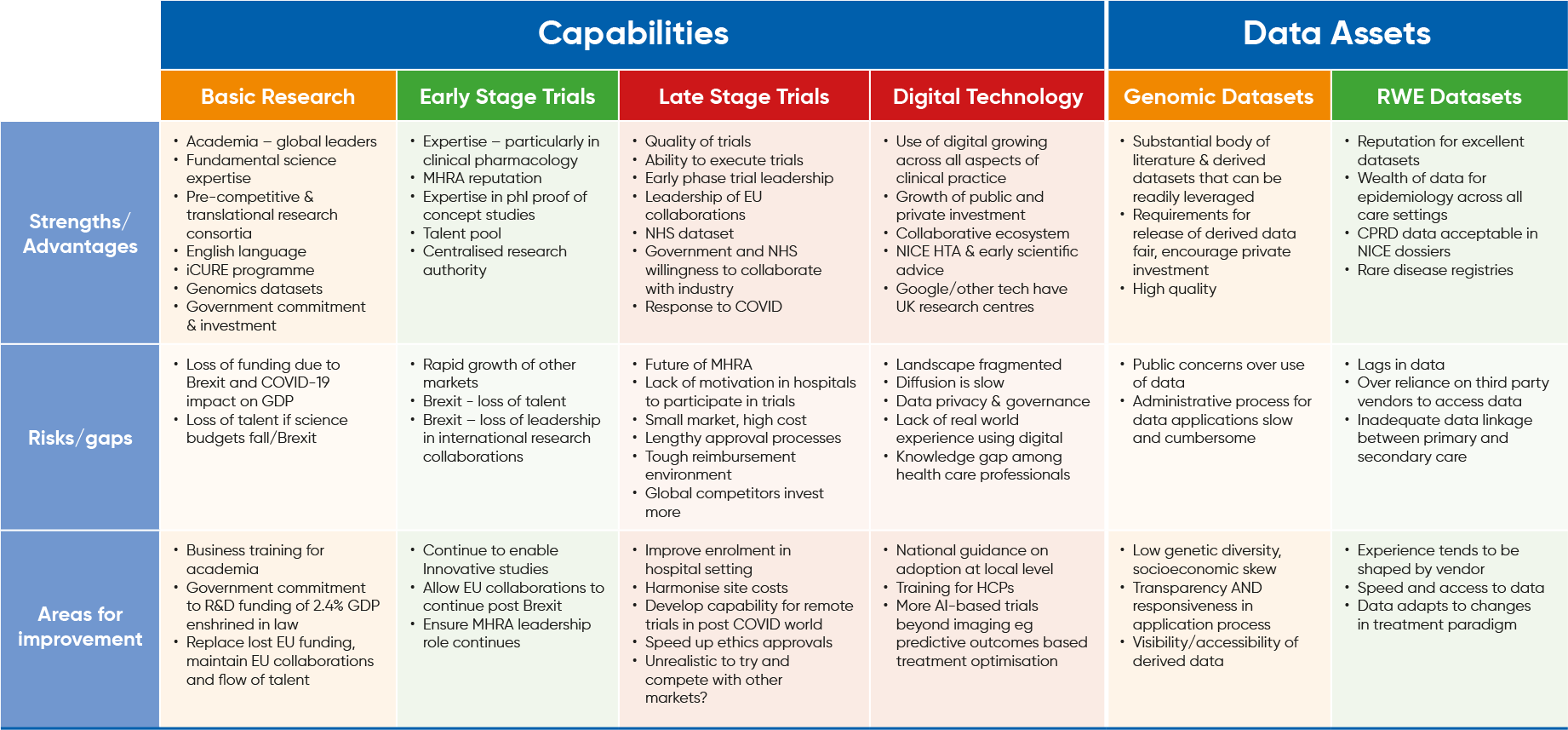

In basic research, the UK has retained its position in the premier league of R&D countries: leading academics, great science, supportive funding institutions, a rich biotech ecosystem and willingness to collaborate.

The UK’s position on late-stage trials has declined since Covid. Recruitment to late-stage trials is decreasing but there are green shoots due to action taken by MHRA to tackle delays and O’Shaughnessy review and implementation.

The UK should continue to leverage its world-leading data. The NHS has taken constructive steps that address the need for greater diversity in UK datasets since our last review.

The digital health landscape in the UK is dynamic and evolving. The combination of innovative start-ups, supportive policies, and robust research and development initiatives places the UK at the forefront of digital health globally.

JPG view of the Life Sciences Ecosystem in the UK 2020

Overall Project Conclusions